Mr & Mrs B and the cost of no planning

Two decades ago, Mr & Mrs B invested £500,000 inherited from the sale of a parent’s house into investment bonds – attracted by the tax-efficient growth.

They didn’t seek further tax advice at the time as they’d already paid inheritance tax on the sum received.

Over the years, they watched as their investment grew steadily up to £2,000,000, confident that this long-term growth would secure a healthy “pot” to eventually pass on to their children.

But as with many long-term strategies, what was appropriate at the outset isn’t always right today.

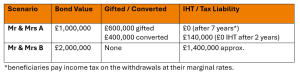

Because without updated planning, the remaining bond value on death would now leave their children facing a significant inheritance tax bill of £800,000. Along with a £600,000 income tax bill on the gains, meaning a large proportion of the bond’s growth being lost.

There will be many other families in the same position, simply unaware that the gains built up inside investment bonds can become liabilities on death.

Even for experienced investors and advisers, this risk often goes unnoticed: it rarely appears on routine tax returns, and financial advisers don’t always flag it unless specifically asked.

But the last thing anyone wants to do is to leave the next generation with a surprise tax bill.

Mr & Mrs A took a more considered approach.

Similarly, having inherited £500,000 20 years ago. They too invested this in an investment bond and drew their 5% allowance each year, tax-free, giving them an extra £25,000 income annually.

After 20 years of growth, despite the income drawn, the bond is now worth £1,000,000.

However, rather than leaving the bond untouched until death, they sought tax advice. And with guidance, they:

- Converted £400,000 of the bond into investment qualifying for IHT relief to replace their 5% annual income.

- They then gifted the remaining £600,000 to their children (by assigning part of the bond), allowing them to pay off their mortgages and utilise their own tax bands.

As a result, the children received funds tax efficiently. This gift will be outside of Mr & Mrs A’s Estates after 7 years, and the qualifying investment will not only provide an additional income throughout retirement for Mr & Mrs A but can also be passed on death to the children, free of inheritance tax, after two years.

This meant that they were able to help out their children at a time that mattered, allowing them to invest confidently for their own futures – and all without inheriting a large, unintended tax liability.

The key numbers at a glance

A further example

We recently encountered a situation which highlights how significant this issue can become if left unreviewed.

An elderly client in their 80s had a modest pension income of around £30,000 per year and had moved into a care home. On their death, it emerged that they held investment bonds worth approximately £1 million which had been accumulated over many years.

Because the bonds had been largely left untouched, their value had grown substantially. However, this meant the bonds formed part of the estate on death and significantly increased the inheritance tax liability.

In situations like this, the tax position can change dramatically simply because large investment bonds have been left to grow for many years without being considered as part of the wider estate planning strategy.

A review earlier in retirement could have allowed part of the bond to be managed and potentially passed on to the next generation more efficiently through lifetime planning.

Could this apply to you?

Many people hold investment bonds without realising the potential inheritance tax implications. These investments were particularly popular 15–25 years ago as a way of allowing funds to grow in a tax-efficient wrapper.

But with a continued squeeze on marginal tax rates through Fiscal Drag, when these investments bonds are realised can materially affect the overall tax paid, particularly when paired with Top Slicing Relief and Time Apportionment Relief.

You may have an investment bond if:

- You invested a lump sum with an insurance company or investment provider

- You’ve been able to withdraw up to 5% of the original investment each year tax-free

- The investment was originally set up through a financial adviser

- Statements refer to “segments” or “chargeable event gains”

For many, these bonds have performed well and have quietly grown in value over the years. However, the tax implications, particularly on death, are often overlooked.

So, if you believe you may have set up an investment bond and have largely left it to grow, then it may be worth reviewing how it fits within your wider inheritance tax planning.

Key takeaways for families with long-term investments

- Review long-standing investment bonds. Even well-established, long-standing strategies need reviewing periodically. What made sense 20 years ago may not be the best plan now.

- Consider lifetime planning: Lifetime planning of investment bonds can protect both capital and heirs, ensuring wealth passes efficiently.

- Plan early: Planning early allows families to control timing and tax impact, rather than leaving children to inherit assets at the worst possible time.

- Include surviving spouses in planning: restructuring can and is often done at natural life milestones.

Small adjustments now could make a significant difference to the next generation -preserving your wealth and making sure it reaches them when it’s most useful, along with giving you the peace of mind that decades of potential growth isn’t unnecessarily lost overnight.

We’re here to help

If this is something that may affect you, then a conversation with us is the best place to start. We can then guide you on the best next steps based on your unique situation.

Call Graham or one of the team on 0330 058 6559 or email hello@scruttonbland.co.uk