Following last October’s Autumn Budget, and the changes announced to Agricultural Property Relief (APR) and Business Property Relief (BPR), the need for expert advice in the agricultural sector has never been more needed.

The proposed changes from 6th April 2026 are set to have massive implications for family farms on everything from inheritance tax (IHT) on family assets to pension planning, Trusts, Capital Gains Tax, farming tenancies – even the vehicles used for the business. And farmers across the country are anxiously trying to take stock of the risks and opportunities in their businesses.

Then there’s the additional changes to National Minimum Wage and Employer National Insurance to think about, with many farms having diversified in recent years and taking on seasonal workers in hospitality and leisure activities.

With so much complexity surrounding the various changes, and the different implications fr individual circumstances, those across the industry are feeling the pressure to act quickly.

Farm owners, especially those running multi-generational family operations, are understandably nervous.

And as advisors, it’s a unique and unsatisfactory position to be in to deliver impactful advice without formal legislation beyond the statement of intent in the October 2024 budget.

However, there are proactive steps farmers can take now to navigate the shifting tax rules and we’ve already seen many real examples that demonstrate how to approach these challenges successfully.

What’s important across the board is not to panic. Whilst there are time-sensitive elements, it’s vital that you make time to make best decision for your circumstances.

Real-Life Farming Family Case Studies

We’ve recently worked on several cases that highlight the impact of these changes on family farms, and how proactive steps can reduce liabilities.

Hopefully by exploring these real-life examples you can see how these tax changes affect businesses in many different ways, and what strategic action can be taken to alleviate some of the burdens.

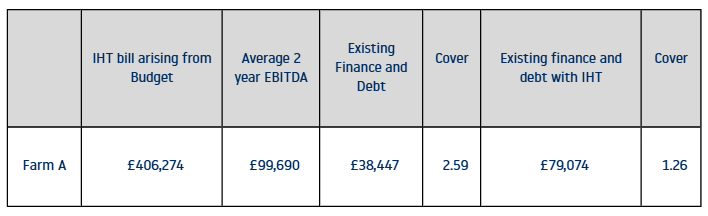

Farm A: Strategic Gifts and Pension Adjustments

- Family Structure: Father (77), son, and daughter-in-law in partnership.

- Farm Operations: Combinable crops and small pig enterprise, spanning 370 acres.

- Current Situation:

- No bank debt, but a hire purchase agreement for a tractor.

- Gift of land to the son, with a Potentially Exempt Transfer (PET) subject to seven years; CGT holdover relief claimed. Wife (76) admitted to the partnership with a joint share in the land and farmhouse.

- Two-year qualifying period for wife to be eligible for APR and BPR exemptions.

- Action Taken:

- Reviewed the profit allocation and revised the partnership agreement.

- Admitted the wife into the partnership to use her £1 million exemption.

- Pension access used to replenish reduced profit following the gift of land.

- Cost & Outcome:

- Professional fees (comprising Land Agent, Accountant and Solicitor) of delivering the services: £12-15k.

- The strategy reduces the IHT liability by over £400k but requires the qualifying periods for exemption to be met

Farm B: Gift with Holdover and Life Insurance Planning

- Family Structure: Parents (84 and 82), son in partnership.

- Farm Operations: Combinable crops and sugar beet on 430 acres.

- Current Situation:

- 290 acres, farmhouse, and buildings owned by parents.

- Existing bank debt secured on the son’s property interest.

- Gift of land to son, retaining house, buildings, and some land; partner capital also gifted to son.

- PET subject to seven years; CGT holdover relief claimed.

- Gift inter vivos planned, along with a decreasing term life insurance policy.

- Action Taken:

- Reviewed profit allocation, equalized partner capital between parents and son.

- Explored life insurance to mitigate the risk of not surviving the seven years.

- Cost & Outcome:

- The strategy helps reduce IHT liability, though the family is weighing up the costs of life insurance policies.

- A more tax-efficient transfer of assets over time.

Farm C: Trust and Family Considerations

- Family Structure: Parents (84 and 81), three children (one on farm, two with off-farm careers).

- Farm Operations: Combinable crops, sugar beet, 700 acres owned, 350 acres under AHA tenancy, plus four residential lets.

- Current Situation:

- Bank loan secured for land purchase.

- Proposed gift of land to son, considering equity between siblings.

- Possibility of using a trust to hold land for all siblings and next generation

- Residual IHT liability arising from non-core residential property.

- Action Taken:

- Engaged in discussions about how each sibling would benefit from the assets depending on ownership structure.

- Explored the possibility of a trust to hold land, digesting the consultation document published on 27th February 2025.

- Most recent residential purchase identified as non-core that could be sold to help cover any residual IHT bill.

- Cost & Outcome:

- Ongoing consultations, with a focus on achieving consensus between siblings before making any significant gifts.

** EBITDA is rent after income tax available to service IHT repayments

** EBITDA is rent after income tax available to service IHT repayments

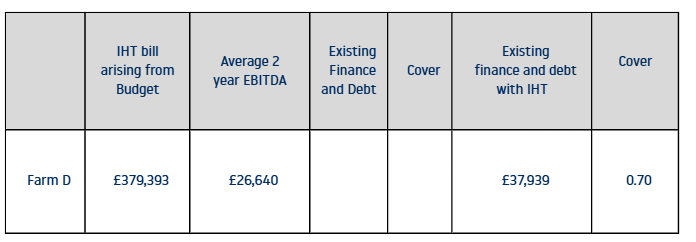

Farm D: Succession Planning and Valuation Considerations

- Family Structure: Parents (75), owning 444 acres let on a perpetual AHA tenancy to family farm company; son owns an additional 306 acres under the same tenancy.

- Farm Operations: Land rented under tenancy, farm company holds a 49% share.

- Current Situation:

- Original farmyard has been improved and let as a business park.

- Gift of the entire landholding to children under PET, subject to seven years; CGT holdover relief claimed.

- Rent income would be forgone, requiring replacement income.

- Action Taken:

- Reviewed succession plans, including gifts with reservation of benefit.

- Discussed potential valuations for land, tenancies, and shares.

- Pension access considered to replace lost income.

- Cost & Outcome:

- Tenancy arrangements need to be carefully examined to determine implications on valuation of land subject to the tenancy and the value of the tenant right.

- Shareholdings can benefit from minority discount in certain circumstances which can be advantageous in reducing value interest in family farming companies.

The figures above are based on real examples of accounts for current clients – with names and details changed to protect privacy.

For the purposes of this article the following calculations and terms have been used:

“Cover” is a ratio that calculates a company’s margin of protection in servicing its debt and making dividend payments.

EBITDA is based on profit excluding depreciation, amortisation, bank interest but after drawings and income tax.

Figures are based on the financial years ending 2023 and 2024 for harvest years 2022 and 2023 (arguably indicating a better than ordinary result given the strength of the 2022 harvest result for most farms)

It should be noted here that average 2 year EBITDA is calculated by taking the profit – adjusted for drawings and tax, as a crude measure of how much cash a business can generate

Key Insights and Considerations for Family Farms

These real-life examples show the importance of proactive tax planning in the face of this evolving legislation. But there are many other considerations such as:

- Proactive Gifting: Farmers can reduce IHT by gifting land or assets, but it’s essential to plan ahead and use exemptions like the £1 million IHT allowance and CGT holdover relief strategically.

- Partnership Agreements: For farms with multiple family members, making sure partnership agreements are aligned with succession goals and tax relief eligibility can make a significant difference.

- Pension and Life Insurance: Accessing pensions to replenish income after making gifts, and exploring life insurance to cover potential IHT liabilities, are strategies that need to be factored into a comprehensive tax plan.

- Trusts as Tools for Equity and Protection: Trusts offer a way to protect assets and provide for future generations, but they come with complexities that require careful planning and professional advice.

- Succession Plans Should Be Dynamic: Succession planning is not a one-time task but a dynamic process that involves constant review, especially when new legislation comes into play.

Further considerations

The legislation is yet to be finalised and there has been much speculation of how the announcements could evolve;

Could there still be an age exemption to consider? Where that line is drawn would inevitably create winners and losers so is it fair?.

Could the £1m exemption amount be increased? Taking this to £5m would change things for a significant number of farms.

Could the tax be calculated but only collected if the inherited asset is sold? This seems an equitable and pragmatic outcome and is favoured by those sector organisations lobbying Government but to date no engagement.

Could there be a possible extension from seven years to ten years? This would further penalize an aged generation that to date has held land for good reason and compound the sense of unfairness of the announcements.

Following the Spring Statement on the 26 March there was no further mention of any of these topics so we wait to see how matters evolve over the summer months before legislation is brought to Government for assent ahead of the 6th April 2026

Next steps

Whether through gifting land, restructuring partnerships, exploring life insurance options, or using trusts, each decision made now will have a lasting impact on the future of your farm.

As agricultural accounting specialists we’re here to support you – the farming community – with navigating the complexities of tax planning, minimising your liabilities, and securing the future of your family businesses for generations to come.

To discuss your individual circumstances, get in contact with Nick or one of the team by calling 0330 058 6559 or email hello@scruttonbland.co.uk

This article was written following the success of our Virtual Farming Briefing event on Thursday 6 March, where experts from across the sector shared their experience and solutions on current challenges in the farming industry. You can watch the recording of this event here (add link to video).