Many businesses need to have company vehicles to conduct their day-to-day work. And when it comes to choosing this vehicle, it’s common to purchase or lease for a period often of around 3 years, so it’s important to choose the type of vehicle that best suits the purpose.

This might be a company car or a commercial vehicle taxed as a van, but before committing to the contract it’s important to consider whether to purchase or lease, and the tax implications both for the employer and the employee over the intended period of use.

Joy Shaw, Senior Tax Adviser outlines the key tax implications to consider.

The Government’s approach to company vehicles

As the government’s strategic approach to taxation continues to evolve, the choice of diesel, petrol, hybrid, electric or other fuel is also an important one.

The previous Conservative government had increasingly encouraged the use of vehicles with a low C02 emission g/km which is reflected in tax charges and incentives.

The Labour government in the first Autumn Budget Statement 2024, stated that they saw the transition to electric vehicles (EVs) as crucial to decarbonising transport – with a vision that new cars that rely solely on internal combustion engines (ICE) will be phased out by 2030, and that from 2035 all new cars and vans sold in the UK will be zero emission.

In their next Autumn Budget Statement 2025, the government acknowledged that battery and plug-in hybrid electric cars pay a lower amount of fuel duty than petrol or diesel cars. And in the case of fully electric vehicles, no fuel duty is liable as they’re not propelled by fossil fuels.

The government has said that although they contribute to congestion and general damage to the road network, electric cars do not contribute to addressing these the way that other drivers do by paying fuel duty.

The growth in use of electric vehicles has also reduced the government’s receipts from fuel duty.

That’s why the government will introduce electric Vehicle Excise Duty (eVED) from April 2028. It will be set at half of the equivalent rate of fuel duty for electric cars, and half again for plug-in hybrid cars.

eVED will ensure all car drivers contribute but will still maintain important incentives to switch to an electric vehicle.

eVED will not require ‘trackers’ in cars, nor will the government ask people to interact with a whole new tax system: car drivers will pay for the miles they drive alongside paying their usual road tax (VED). The government has now launched a consultation on this proposal.

The government’s car policy is to be supported by:

- Investment in accelerating EV charge point roll out.

- Introducing a plug-in vehicle grant for the purchase of new electric vans

- Supporting the manufacture of wheelchair accessible EVs

- Introducing eVED from April 2028

- Maintaining tax incentives to invest in EVs

Lower Vehicle Excise Duty First Year Rates

The Vehicle Excise Duty, Expensive Car Supplement threshold was raised in the 2025 Budget from £40,000 to £50,000 which affects licences (that are not the first licence) that come into effect on or after 1 April 2026 and will apply to zero emission vehicles registered from 1 April 2025 onwards.

Company Car Tax Regimes

Extending 100% first year allowances for EVs and charge points by one year to 31 March 2027 for Corporation tax purposes.

Company car tax rates have already been announced for 2028-29 and 2029-30 which will provide some certainty, but the trend is upwards for all types of vehicles, so even driving a fully electric company vehicle can become more expensive.

Fully electric cars that had a benefit-in-kind (BIK) rate of 2% in 2024/25 will rise to 5% by 2027/28, to 7% by 2028/29 and to 8% by 2029/30.

The highest BIK rate (currently 37% up to 2027/28) will be charged on more vehicles as the CO2 g/km threshold is reduced and the BIK percentage will be increased to 38% in 2028-29 and to 39% in 2029-30.

Rates for hybrid vehicles will rise to align more closely with internal combustion engine (ICE) vehicles.

Double cab pick-up vehicles, that had previously enjoyed the beneficial tax treatment as a van, have been taxed as a company car since April 2025. But transitional relief is available until 5 April 2029 for existing vehicles contracted up to 5 April 2025.

It’s likely there’ll be a reduction in the popularity of double cab pick-ups moving forwards as they become a more expensive benefit in kind.

What are the key considerations when choosing a company vehicle?

Once the type of vehicle has been tentatively chosen, the tax implications are the next consideration. These are the main points to bear in mind:

- Income Tax

- Company Van

- Keeping a company vehicle at home

- Company Car Fuel Benefit

- Company Van Fuel Benefit

- Electric Charging

- Corporation Tax

- Relief for Unincorporated Businesses

- Leasing of motor vehicles

- Planning for the Future – Electricity and Hydrogen

Income tax

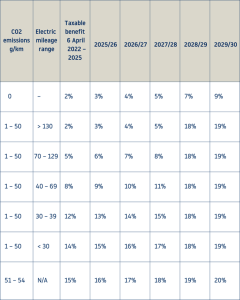

A company car or van is regarded by HMRC to be a non-cash reward for the employee, or a benefit in kind (BIK). This means that tax needs to be paid by the employee on this – referred to as a taxable benefit. The taxable benefit is calculated from the list price of the car multiplied by the taxable benefit %.

This % is determined by the CO2 emissions of the car and the electric mileage range: the lower the emissions and the higher the electric mileage, the less tax is due.

Announced in the Autumn Budget Statement 2024 and updated in 2025:

- Appropriate Percentages (APs) for zero emission and electric vehicles will increase by 2 percentage points per year in 2028-29 and 2029-30, rising to an AP of 9% in 2029-30.

- APs for cars with emissions of 1 – 50 g of CO2 per kilometre, including hybrid vehicles, will rise to 18% in 2028-29 and 19% in 2029-30. There was however a temporary easement announced in the November 2025 Budget Statement where new EU and UN emission standards observe higher C02 emissions for PHEVs than previous standards.

- APs for all other vehicle bands will increase by 1 percentage point per year in 2028-29 and 2029-30. The maximum AP will also increase by 1 percentage point per year to 38% for 2028-2029 and 39% for 2029-2030. This means for vehicle bands with emissions of 51 g of CO2 per kilometre and over, APs will increase to 19% – 38% range in 2028-29 and 20% – 39% range in 2029-30.

Company Vehicle Appropriate Percentage rates for the period 6 April 2022 to 5 April 2030

For company cars with CO2 emissions exceeding 54 g/km the employee’s taxable benefit increases by 1% for every 5 g/km up to a maximum of 38% in 2028-29 and 39% in 2020-30. Diesel cars that do not meet the RDE2 standard are also subject to a 4% supplement.

The taxable benefit will depend on the vehicle and will be taxed as employment income at the employee’s marginal rate of income tax.

For example, a company car with CO2 emissions of 30 g/km and an electric range of 50 miles would have a taxable benefit of 8% when it was bought in 2024/25 but that would increase to 19% in 2029/30. If the car had a list price of £35,000 the benefit-in-kind value for the tax year would be £2,800 in 2024/25, rising to £6,650 in 2029/30.

For this reason, as cars age, the taxable benefit is likely to increase, (which is somewhat counter intuitive), so the company car fleet needs to be kept under review.

As a result, a higher rate taxpayer with a marginal tax rate of 40% would pay £1,120 of income tax for the year 2024/25, compared to £2,660 for private use of the same company car in 2029/30.

If the employee contributes towards the purchase of their company car (classed as a capital contribution), this will reduce the list price for these purposes, resulting in less tax to pay, however the maximum deduction that can be made is £5,000.

Company van

Company van benefits are calculated as follows:

CO2 emissions 0g/km | Taxable benefit £0

Anything above 1 g/km | Taxable benefit £4,020 for 2025/26 / £4,170 for 2026/27

Calculating a company van taxable benefit is a much simpler process because the list price, CO2 emissions and electric mileage range are not considered.

As with company cars, the taxable benefit on a van will be taxed as employment income at the employee’s marginal rate of income tax. However, if a company van is used privately, and the usage is insignificant or if it’s only for commuting purposes, then no taxable benefit arises.

HM Revenue and Customs defines a van as “a vehicle primarily constructed for delivering goods with a fully laden gross weight of 3.5 tonnes.” It is designed as a vehicle primarily suited for the conveyance of goods of any description.

However, as mentioned before – the change in the classification of double cab vehicles from a van to a car, makes these a more expensive option.

Keeping a company vehicle at home

A company car used by an employee and kept at their home overnight is deemed by HMRC to be available for private motoring, which includes home to work commuting. This means a taxable benefit will be incurred by the employee.

In contrast, a van can be taken home overnight, and if no other significant private motoring is undertaken in the vehicle, home to work site commuting will not create a taxable van benefit for the employee.

Company car fuel benefit

Where the employer pays all the fuel costs, (including private journeys) a separate taxable benefit arises, unless the employee reimburses the employer in full for the fuel used for private motoring.

Where the employee pays for all the fuel and the employer reimburses them only for the business fuel cost, no taxable benefit will arise on the employee.

As with the company car benefit, the car fuel benefit is subject to income tax, which the employee will pay at their marginal tax rate.

To calculate the taxable benefit, the following formula is used for the 2026/27 tax year:

£29,200 x “taxable benefit %”

Company van fuel benefit

The van and van fuel benefit charges have been increased in line with the UK Consumer Prices Index (CPI) with effect from 6 April 2026.

If free or subsidised fuel is provided to the employee for private use in a company van, they will be taxed on a van benefit of £798 for the 2026/27 tax year, at their marginal rate of income tax. There is no reduction in the taxable benefit where an employee makes a contribution towards private fuel for the van.

Vehicle excise duty on electric vehicles

The government uprated standard Vehicle Excise Duty (VED) rates for cars, vans and motorcycles, excluding first year rates for cars, in line with the Retail Price Index (RPI) from 1 April 2026.

VED First Year Rates

VED First Year Rates for new cars have been changed to strengthen incentives to purchase zero emission and electric cars, by widening the differentials between zero emission, hybrid and internal combustion engine (ICE) cars.

- Zero emission cars will pay the lowest first year rate at £10 until 2029-30

- Rates for cars emitting 1-50 g/km of CO2, including hybrid vehicles, have increased to £115 for 2026-27

- Rates for cars emitting 51-75 g/km of CO2, including hybrid vehicles, have increased to £135 for 2026-27

- All other rates for cars emitting 76 g/km of CO2 have significantly increased from historic rates, so it’s worth checking these in advance.

Electric charging

Where electric charging is made available to an employee at their place of work – provided this is available to all employees – this is a tax-free benefit and no benefit-in-kind charge arises, regardless of their level of private mileage.

In addition to this, where an electric company car is provided to an employee and an electric car charger is installed at their home, the cost of installing this is also tax free. However, if the employer pays to install an electric charger at an employee’s home for the employee’s private vehicle, this will result in an income tax liability on a taxable benefit for the employee at their marginal tax rate.

Special rules apply to electricity used to charge a fully electric company car, as it is not regarded by HMRC as a “fuel”, and the HMRC guidance in this respect continues to evolve.

Corporation tax

Businesses purchasing company cars are eligible for a Corporation Tax deduction. It will need to be claimed as a capital allowance on the purchase, which means part of the value of the car can be deducted from a business’s profits before they pay tax. The current tax relief is:

| CO2 emissions g/km | Taxable benefit |

| 0g/ km | £0 |

| Up to and including 50g/km

Used 0g/km |

Writing Down Allowances at 14% from 1 April 2026

of the car’s value per year (a reduction from 18%) Hybrid rate for periods that span the change. |

| Above 50g/km | Writing Down Allowances at 6% of the car’s value per year |

The 100% First Year Allowances for zero emission cars is in place until 31 March 2027.

Vans and commercial vehicles are classed as qualifying assets for Annual Investment Allowance (AIA) purposes. This means that tax relief can be claimed at 100% of the purchase price, provided sufficient AIA is available. The AIA limit is currently £1m.

Full expensing relief at 100% has been introduced permanently for companies, which will apply once the AIA has been fully utilised.

Tax advice will need to be taken in relation to the claiming of allowances by Groups.

If the benefits provided to employees are not included within their payroll, then a P11d must be submitted to HMRC by 6 July following the end of the tax year. Class 1A NIC is due to be paid by the employer at a rate of 15% for the 2025/26 tax year, on the value of benefits provided to employees. This is payable to HMRC on or before 22 July following the end of the tax year.

Relief for unincorporated businesses

Sole-traders and partnerships are also able to claim Capital Allowances on the purchase of cars as detailed above, but the first-year allowances can only be claimed by companies.

Leasing of motor vehicles

If instead of purchasing a vehicle, a leasing arrangement is entered into, the costs incurred in leasing it are treated as allowable revenue expenditure and therefore no Capital Allowances can be claimed on these vehicles.

The type of lease entered into will determine the expenses that are tax deductible.

There are two ways in which you can lease an asset: an operating lease or a finance lease.

- If the lease is an operating lease, then the total expense will be the lease rentals that are shown in the profit and loss account, subject to the potential restriction noted below.

- If the lease is a finance lease, then the total expense will be the finance lease interest and the finance lease depreciation figures that are shown in the profit and loss account.

Where a car is leased with CO2 emissions exceeding 50g/km, a lease rental restriction applies. This means that 15% of the expenses are disallowed for tax purposes as the lease relates to a high emission car.

The treatments of lease arrangements are the same for companies, sole-traders, and partnerships.

Planning for the future – electricity and hydrogen

As part of the wider transition to low-carbon transport, alternative fuels such as hydrogen are also being developed alongside electric vehicles. Businesses with longer-term fleet planning considerations may therefore look at emerging infrastructure and technology in this area.

Freeport East Hydrogen Hub is located at Harwich and is part of the Government’s decarbonisation scheme strategy.

At its anticipated peak by 2030 the aim is to produce 1GW of hydrogen from this site, enough to fuel over 500,000 vehicles.

Which company vehicle is right for me?

Choosing the right company vehicle is no longer a straightforward decision, with tax costs, environmental policy and future legislative changes all playing an increasing role.

While electric vehicles continue to benefit from favourable tax treatment, these advantages are gradually reducing, and the overall cost of providing company vehicles is expected to rise.

Businesses should therefore regularly review their vehicle strategy, taking into account both the immediate tax implications and longer-term changes to ensure they remain efficient and fit for purpose.

We’re here to help

To discuss the taxation of company vehicles within your business talk to Joy or one of our tax team by calling 0330 058 6559 or email hello@scruttonbland.co.uk